All Categories

Featured

Table of Contents

Adjusting to the Financial Realities of 2026

The economic shifts of 2026 have introduced brand-new variables into the math of personal finance. High rate of interest and altering work patterns indicate that conventional methods of preserving a high credit report frequently fall brief. Families throughout the nation now deal with a truth where credit schedule is tighter and scoring designs are more conscious small modifications in spending behavior. Understanding these shifts is the very first step towards rebuilding a monetary foundation that can withstand future volatility.

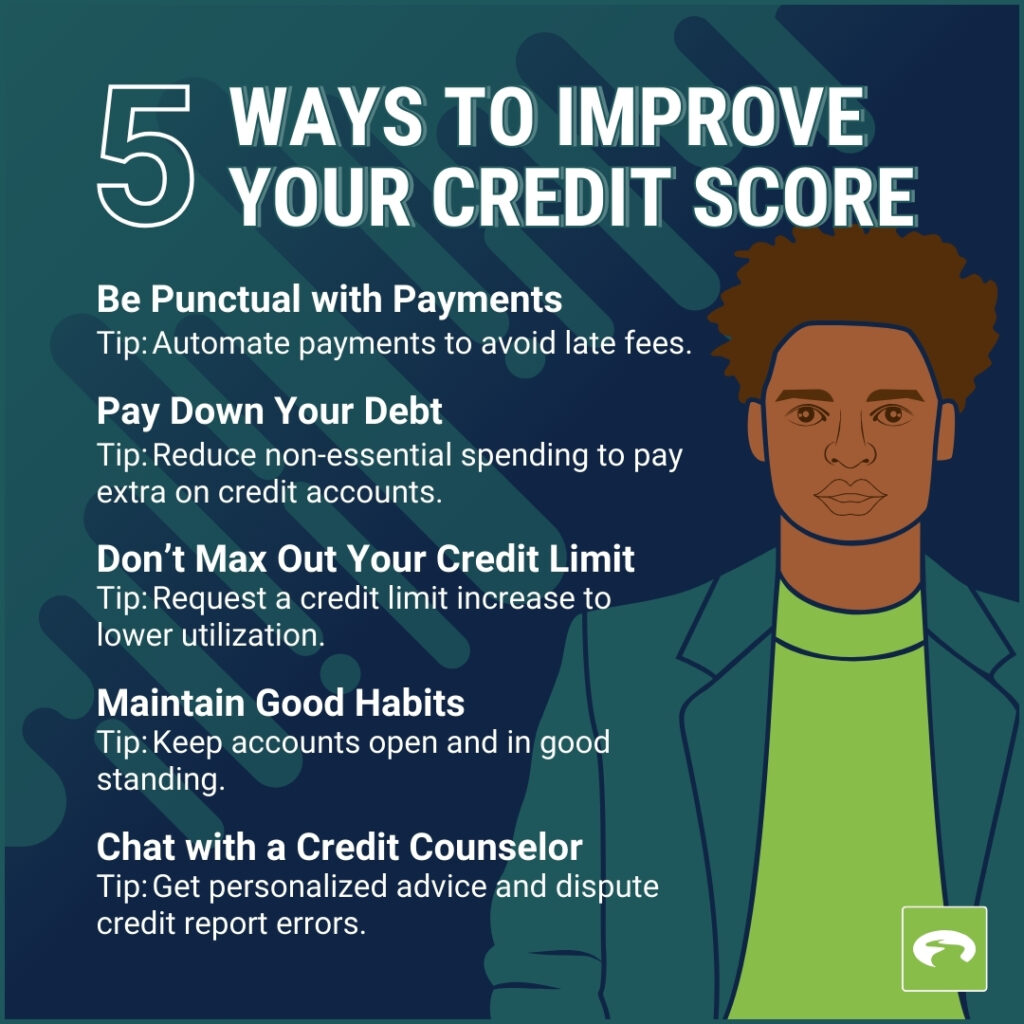

Credit report in 2026 are no longer just a reflection of whether bills are paid on time. Modern scoring algorithms now place heavier emphasis on the ratio of debt to readily available credit and the frequency of brand-new credit questions. For citizens in Pasadena Credit Counseling, staying ahead of these changes needs a proactive approach to debt monitoring. Lots of individuals find that even small oversights on little accounts can cause disproportionate drops in their total score, making it more difficult to protect real estate or automobile loans.

Strategic Budgeting in Pasadena Credit Counseling

Budgeting in the current year needs a level of precision that was less important in the past. The increase of subscription-based services and variable utility costs has made it hard to track every dollar without a structured strategy. Effective monetary management in 2026 includes categorizing expenditures into repaired needs and flexible expenses while strictly restricting the use of high-interest revolving credit. Keeping focus on Credit Counseling typically yields long-lasting benefits for those attempting to recuperate from previous financial downturns.

A typical method includes the 50/30/20 guideline, though lots of monetary consultants in 2026 recommend adjusting these percentages to account for greater housing costs. Designating 50 percent of earnings to needs, 30 percent to wants, and 20 percent to financial obligation payment or cost savings offers a clear map for day-to-day costs. In the region, where regional economic aspects vary, customizing this ratio to fit specific cost-of-living adjustments is essential for sustainable growth.

The Role of Credit Therapy and Professional Oversight

Navigating the intricacies of the 2026 credit market often requires outside expertise. Organizations like APFSC.ORG run as U.S. Department of Justice-approved 501(c)(3) nonprofit credit counseling companies. These entities provide a range of services developed to help people restore control without the predatory costs typically associated with for-profit repair companies. Their offerings include complimentary credit counseling, financial obligation management programs, and pre-bankruptcy therapy. Due to the fact that they are nonprofit, the focus stays on the financial health of the client rather than the bottom line of the firm.

Financial obligation management programs are especially efficient in the existing high-interest environment. These programs work by consolidating various monthly commitments into a single payment. The agency works out straight with creditors to decrease rate of interest, which can significantly reduce the time required to end up being debt-free. Local Credit Counseling Services provides structured assistance for those overwhelmed by month-to-month responsibilities, making sure that every payment made goes even more toward decreasing the principal balance.

Improving Ratings through Controlled Debt Management

When a person goes into a financial obligation management strategy, the goal is to show creditors a consistent pattern of dependability. While these programs sometimes need closing specific credit accounts, the long-lasting effect on a credit score is usually positive since it eliminates late payments and minimizes overall debt levels. By 2026, financial institutions have actually ended up being more going to deal with not-for-profit firms since it increases the likelihood of recovering the funds owed. This cooperation benefits the customer by providing a clear course out of high-interest traps.

Financial literacy stays a foundation of the services supplied by these firms. Education on how interest compounds and how credit usage affects ratings allows individuals to make much better options as soon as their financial obligation is under control. People living in Pasadena Credit Counseling can access these resources through local partnerships between national nonprofits and neighborhood groups. This localized technique makes sure that the advice provided reflects the specific financial conditions of the region.

Real Estate Stability and HUD-Approved Counseling

Real estate remains one of the largest monetary obstacles in 2026. For those aiming to purchase a home and even rent a new apartment or condo, a credit rating is often the primary gatekeeper. HUD-approved real estate therapy uses a way for possible house owners to get ready for the home mortgage procedure. These counselors assess a person's monetary scenario and offer a roadmap for improving credit to meet the requirements of modern lending institutions. Citizens in the immediate region often rely on Credit Counseling in Pasadena to browse credit repair particularly tailored towards realty goals.

Beyond buying, real estate counseling also assists those dealing with foreclosure or eviction. By serving as an intermediary between the homeowner and the loan provider or property owner, therapists can in some cases discover alternatives that safeguard the person's credit history from the disastrous effect of a legal judgment. This kind of intervention is a critical component of the across the country services offered by companies like APFSC, which maintains a network of independent affiliates to reach varied neighborhoods throughout all 50 states.

Long-term Practices for Monetary Resilience

Rebuilding credit is not a one-time event but a series of little, consistent actions. In 2026, the most resistant individuals are those who treat their credit history as a living document. Checking reports routinely for errors is vital, as the automation of credit reporting has led to an increase in technical mistakes. Challenging these mistakes through the correct channels can result in instant score enhancements with no change in real costs routines.

Diversifying the types of credit held is another technique used in 2026 to boost ratings. While carrying a balance is not suggested, having a mix of revolving credit and installation loans shows a history of handling various kinds of debt. For those starting over, secured credit cards have actually ended up being a standard tool. These cards need a cash deposit that serves as the credit limitation, allowing the user to build a payment history without the threat of overspending.

The economic shifts of 2026 have proven that financial security is never guaranteed. By utilizing the resources supplied by not-for-profit agencies and adhering to rigorous budgeting concepts, it is possible to maintain a strong credit profile. Whether through financial obligation management, financial literacy education, or real estate therapy, the tools for healing are readily available to those who seek them. Consistency and informed decision-making remain the most efficient ways to navigate the existing financial environment and prepare for whatever financial changes might follow.

{kind=link}

Latest Posts

The Future of Debt Management for Modern Customers

Finding Trustworthy Debt Advice in Your State

Weighing the Pros and Cons of Credit Therapy Solutions